The number that is closest to their right index finger (the ball has numbers on it) corresponds to a question about spending habits. There are starred categories that are “musts”, so your student has to spend some beans on those. They read up on their salary information, budgeting information, and general financial information. Each avatar is at a different stage in their career, and in a different stage of life (so lots of possibilities to play several rounds of this). Laurie Blank is a blogger, freelance writer, and mother of four. She’s psyched about teaching others how to manage their money in a way that aligns with their values and has been quoted in Bankrate.

Carrie Elle’s Cash Envelope Budgeting for Kids

- However, just like in real life, you can’t just spend all your income on paying down debt.

- From learning how to rent an apartment, to learning how to decide on a big purchase decision – these lessons help prepare teens for real-life scenarios they’ll face in a few short years.

- You’ll get access to an Emergency Fund Savings Tracker worksheet, a Bill Pay checklist, and more.

- It offers affordable pricing, free international calling to over 90 countries, and more.

- A fun activity to kick off money lessons or a money unit would be to have your students go through this Reality Check calculator.

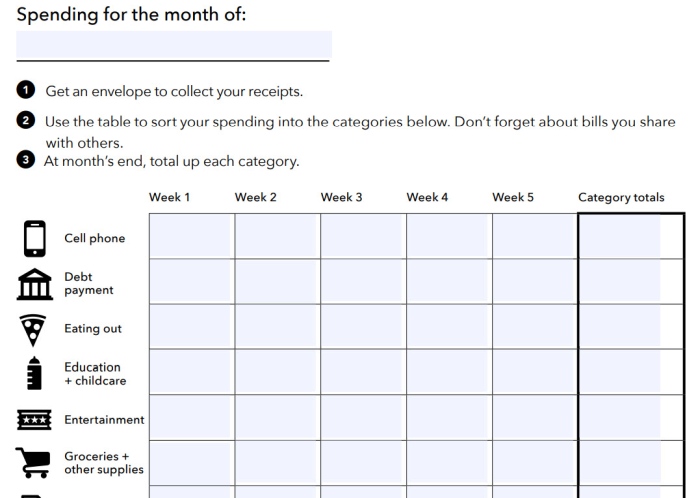

- Whether you are just learning to budget or you don’t need or want all the bells and whistles of fancy software or online budgeting tools, I give you my Really Simple Budget Worksheet.

I mean that they’ll plan (at least a tiny bit) ahead of when they make a transaction with their money. It’s always good to understand the end goal (even if your students won’t reach these for years into the future). Then, have them work through these worksheets to understand how to make large-purchase decisions better. Paying bills is a critical adult money skill…yet I’ve seen hardly any lessons around this. Students will review what various college payment choices are out there, and learn about each (such as scholarships, grants, loans, etc.). I’ve got a whole article filled with the best (free) worksheets, PDFs, and activities I could find having to do with the famous TV show, Shark Tank.

What is it Worth Saving For?

Budgeting is the process of creating a plan involving anticipated revenue and estimated expenditure. Anticipated revenue here is the potential cash inflow for an individual, and the estimated expenditure can be defined as the outflow of the cash for the future. It is the act of balancing one’s expenses with the current income. Budgeting is instrumental for the foundation of any financial plan, and efficiency in financial management behavior is important to make these decisions.

Your money deserves more than a soundbyte.

This is TD Bank’s free printable resource with activities to teach teens how to balance a checkbook. Dallas Fed has a great series of resources around helping students learn how to build wealth. Ask learners to bring in three receipts from recent purchases to use in this wants vs. needs game. To prepare for this game, label one paper lunch sack as wants, and another as needs. When the learners arrive in class, ask them to place their three receipts on their desk. If the receipt contains more than one object, ask the student to circle or highlight one of the objects.

If you have a favorite finance game that would fit on this list, let us know by using our contact page. Money Magic was created to help teach budgeting skills to young adults. You play as the main character, Enzo the magician, and you are working on budgeting to save up a total of $50k for your move to Vegas and venue funds to perform while there.

How to Teach Budgeting (from Beginner to Advanced Levels)

They get to answer various questions (there are only 10) about the type of lifestyle they want to live, and then fill out estimated amounts they think they’ll spend each month for specific budget categories. A fun activity to kick off money lessons or a money unit would be to have your students go through this Reality Check calculator. This budgeting worksheet for students (pdf) was originally part of my Money Prodigy Online Summer Camp, but I’m carving it out for you to use, for free. This cool online game assigns you a career (or lets you choose one) and tailors your experience to your location. You get to make choices about housing and other expenses, and the game calculates how those things fit into a responsible budget.

This set also comes with an end-of-the-month check-in to see how you did progress wise. This home organization printables website offers a host of other printables, articles, a small business guide to payroll management and courses to help you create a peaceful and organized home. Cash envelopes help ensure you stick to your budget by using cash only for discretionary spending.

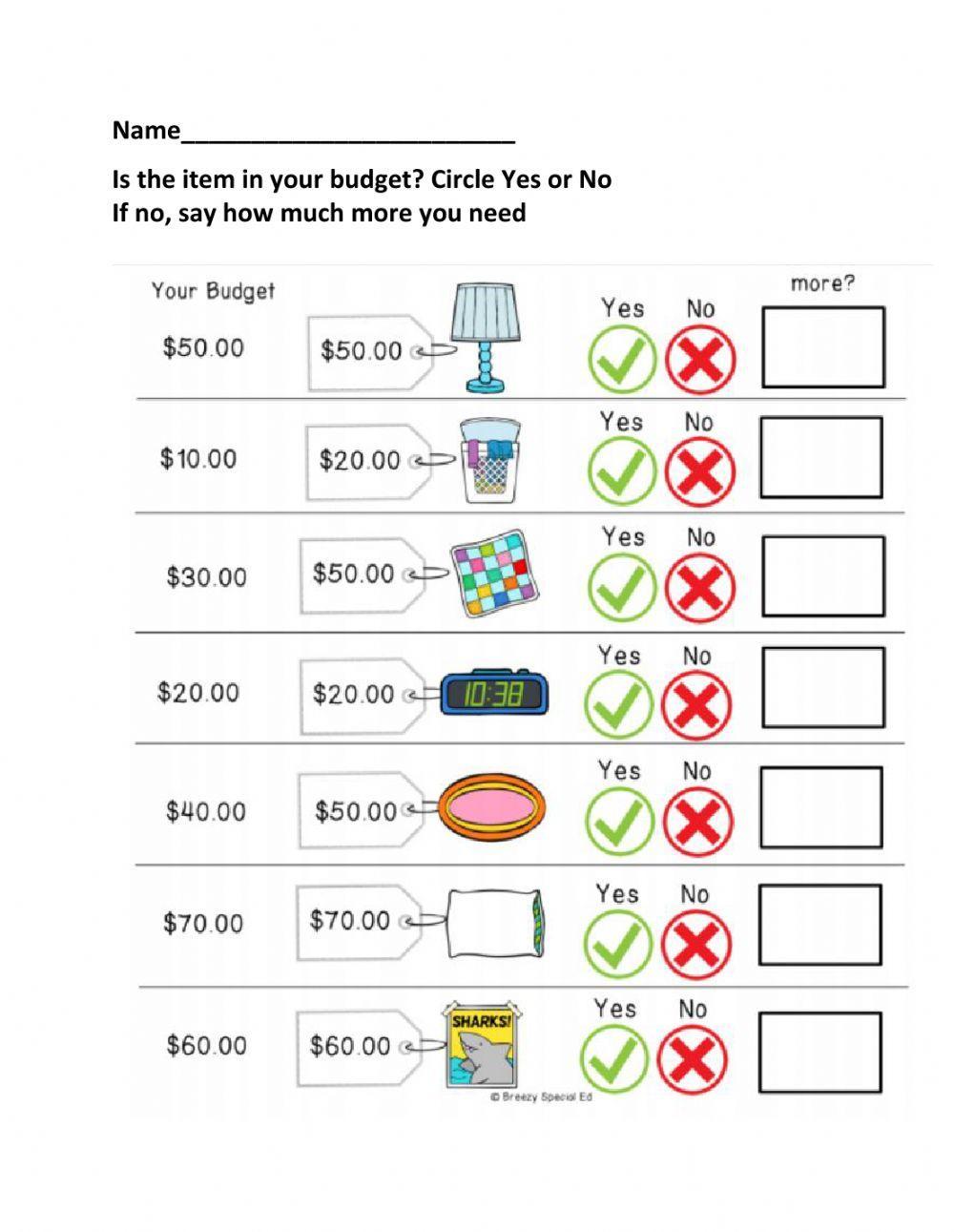

We’re changing things up with this children’s budget worksheet, which allows you to teach your child to budget just three categories. Could be a great way to start, especially if your kid is still saving money in mason jars. That’s a lot – and you typically won’t find spots on teen and kid budget worksheets to support them learning these skills. When the learners arrive in class, divide them into two teams. Write the number that you reached by adding the necessary objects on the board. Explain to the adult learners that they have just been placed on a fixed income and that they only have the amount of money written on the board available to spend.

Please consult with a licensed financial or tax advisor before making any decisions based on the information you see here. Opinions expressed here are the author’s alone, not those of any bank or financial institution. This content has not been reviewed, approved or otherwise endorsed by any of these entities. You’ll get access to an Emergency Fund Savings Tracker worksheet, a Bill Pay checklist, and more. The second step I took was probably the most life-changing as far as our money was concerned.